Who is overrated by Aauto Quicker?

Wen | Jing Yu

Editor | Yang Xuran

Produced by | tide-biz

On February 5th, Aauto Quicker (HK:01024) with the aura of "the first short video" went public. On the first day, its share price rose by nearly 200%, and its market value exceeded one trillion. At that time, the market value of Aauto Quicker was almost the same as that of the whole A-share media industry. Industry observers exclaimed: Aauto Quicker is not crazy, the market is crazy.

Aauto Quicker Stock Price Performance (February 5, 2021-present)

The crazy market gradually calmed down. With the collective withdrawal of technology stocks in the Hong Kong market, Aauto Quicker’s share price quickly halved. By the close of June 3rd, the market value of Aauto Quicker had reached HK$ 850 billion.

The same lopsided decline also occurred in companies such as New Oriental Online, Mingyuanyun and Weimeng. However, due to the large size of Aauto Quicker, the impact on the index is more obvious. Some investors even complained that the Aauto Quicker family had implicated the entire Hang Seng Science and Technology Index.

The high valuation of the capital market is equally important for technology Internet companies listed on A-shares, US stocks and Hong Kong stocks, which is almost the smartest fund in the world to cast a vote of confidence in the company’s development. But high valuation will naturally bring higher expectations-enterprises need to prove that they deserve it with performance.

Although the performance of Aauto Quicker’s latest quarterly report is acceptable, investors still choose to vote with their feet. On the second day after the financial report was released, Aauto Quicker’s share price fell by 11.46%, and its market value evaporated by 100 billion in one day.

For a content-based platform company, user base and commercialization efficiency are two important growth engines. No matter which one is accelerated, it can drive the performance and valuation of the platform to a new level.

However, it is not difficult to find out from the analysis of Aauto Quicker’s financial report that the chronic problem of user growth in Aauto Quicker has not been solved. Juchao has hinted at this in the articles "Aauto Quicker Left Behind" and "Hot Subscription and User Loss: AB Side of Aauto Quicker Listing". However, the improvement of commercialization efficiency of advertising, e-commerce, etc. is still weak corresponding to the current marketing rate (PS) of nearly 12 times.

Before the listing of Aauto Quicker, even the most optimistic analysts only dared to predict that "Aauto Quicker will be able to challenge the market value of 1 trillion within one year of listing", but the greed of generate, the market sentiment, far exceeded the wildest imagination of analysts. The market value on the first day of listing has become a heavy burden on Aauto Quicker, but to return to the peak and cross it, Aauto Quicker’s achievements are far from enough.

A preliminary study on "the first short video"

From the IPO price of HK$ 115 (with a total market value of about HK$ 4,400), it is not difficult to see that Aauto Quicker management and underwriting investment banks are conservative in their valuation. The tripling of the IPO price on the day of listing also means that the IPO price in Aauto Quicker is set low, which fails to maximize the financing benefits of listing.

Aauto Quicker management’s judgment is consistent with the attitude of many institutional investors. The capital market is used to the logic of "the boss gives a premium". As the second child in the industry, Aauto Quicker seems to have no reason to enjoy too high valuation.

But the sky-high price still appeared. On the one hand, liquidity was loose at that time, market sentiment was restless, and high-quality assets were pursued; On the other hand, ByteDance has not been listed yet, and Aauto Quicker, as the "first short video stock", is really scarce. If you are optimistic about or configure a short video track, Aauto Quicker is the only choice.

At present, among all kinds of content platforms, short video is almost the best business model: users upload content at low cost and do not need to buy expensive copyrights in large quantities like long videos; Users are very sticky, and it is difficult to leave after using them; The ability to seize the user’s time is very strong, and it can’t stop with a brush; There are various ways to realize cash-live broadcast, e-commerce, advertising, etc.

Especially in the environment where the dividend of consumer Internet is exhausted and the growth of users is at its peak, all platforms are competing for the same number of users and duration. As a more "advanced" form of commercialization, short videos crush long videos in terms of user stickiness and duration, and even erode users’ use duration in instant messaging applications, that is, WeChat.

At the 9th China Internet Audio-visual Conference, Sun Zhonghuai, vice president of Tencent, commented that some short videos with low intelligence and vulgarity "consumed a lot of users’ time", "subtly impacted users’ ideas" and "lowered users’ minds" caused a heated discussion. Behind this, in fact, whether it is Tencent Video, iQiyi or WeChat, there is a challenge that the user duration is taken away by the short video platform.

Today, Aauto Quicker can still enjoy a valuation close to 12 times the market-to-sales ratio, which largely represents the optimistic view of the capital market on the short video business model. Aauto Quicker, the "first short video", also set an example for the valuation level of the whole industry.

Vigorously failed to work miracles.

However, despite its excellent track and business model, Aauto Quicker still faces a serious growth problem-the scale of users seems to have hit the ceiling. 500 million MAU may be a difficult barrier for Aauto Quicker to break through.

User scale is the basic disk of a content platform. If there is no huge user base, whether it is advertising, live broadcast, e-commerce or financial services, it will only be "without rice".

If the content platform is likened to a water cup that is receiving water, the tap keeps getting water (adding users), and at the same time, there is a leak under the water cup that keeps flowing out (losing users). If the inflow is greater than the outflow, the water level, that is, the user scale, will rise. On the contrary, the user scale will decline.

In order to stabilize the basic disk or increase the number of users, many platforms will burn a lot of money to innovate and promote life. The so-called "miracle" is typical of the original interesting headlines and crazy investment for short-term user growth. This method can indeed achieve obvious results in the short term, but after stopping burning money, users may accelerate the loss.

Aauto Quicker once had a fall on this issue. Last year, Aauto Quicker spent a lot of money to reach an exclusive cooperation with the 2020 CCTV Spring Festival Gala. It is reported that the sponsorship fee for this Spring Festival Gala in Aauto Quicker is the highest since the statistics were published. However, this cooperation promoted Aauto Quicker’s daily life to a higher level in a short time, but it soon fell back.

According to public data, around the Spring Festival in 2020, the daily living of Tik Tok and Aauto Quicker will be around 400 million and 300 million respectively. According to the data of August, 2020, Tik Tok has more than 600 million daily active users, almost twice as many as Aauto Quicker Daily Live.

With huge investment in promotion, Aauto Quicker also broke the profit situation for three consecutive years in 2020, resulting in a loss of 6.348 billion. At the same time, the cash flow generated by its operating activities has also turned from positive to negative.

In the first quarter of this year, Aauto Quicker continued the practice of burning money for users. The data shows that Aauto Quicker’s single-season marketing expenses are 11.66 billion yuan, accounting for 68.5% of its total revenue. This figure has almost caught up with Pinduoduo, which is famous for burning money, and its sales and marketing expenditure in the same period was about 13 billion yuan.

The huge operating expenses have led to the continuous expansion of Aauto Quicker’s losses. Its adjusted net loss in the first quarter was about 4.9 billion yuan, compared with 4.3 billion yuan in the same period last year.

However, Aauto Quicker’s great efforts did not produce a miracle. In the first quarter of this year, both DAU and MAU in Aauto Quicker achieved growth, with DAU reaching 295.3 million, up 16.5% year-on-year, and MAU reaching 519.8 million, up 5% year-on-year. Compared with the huge expenditure, it is not worth mentioning-nearly 11.7 billion has gained 44.1 million new monthly users, and the average cost of each new monthly user is 264 yuan.

With regard to the problem of user growth in Aauto Quicker, Juchao suggested in the previous two articles that the reasons behind this include the homogenization of Aauto Quicker, Tik Tok and the substitution of Aauto Quicker, the network effect of short video platforms with social attributes, the difficulty of attracting users in high-tier cities by the ecology (and reputation) dominated by users, the saturation of users in the short video market, and the competitive impact from WeChat video numbers.

What is certain is that Aauto Quicker will face the pressure of losing users without burning money to promote new activities. However, if we continue to burn money, Aauto Quicker will face the problem of increasing losses, and investors’ worries will also increase.

Invisible ceiling

The practice of changing users by burning money is not unsustainable. Just like in Pinduoduo at the beginning, if users can continue to stay, and contribute enough income to the platform or drive other users to join the platform to form a positive cycle, it is a benign growth model.

There is a very key measure on this issue, that is, ROI (Return on Investment). This index requires spending money to obtain the customer acquisition cost generated by the user, which can not be lower than the life cycle value generated by this user in the long run, that is, LTV≥CAC.

In view of the long-term dynamic of this indicator, we compare the income contribution and cost of single-month users in that year, and we can find that the growth of users and income in Aauto Quicker can’t keep up with the soaring speed of cost.

The main reason behind this is that the commercialization efficiency of Aauto Quicker has not been fully developed, and there is still potential for growth. For example, e-commerce business and advertising business are growing rapidly, while local life business has just started.

Therefore, the current capital market chooses to accept its short-term losses and the disproportion between input and output, and bet on the future commercialization efficiency of Aauto Quicker.

But there are conditions for this tolerance. In the case of disproportionate input and output, once the commercialization efficiency cannot be improved rapidly, the confidence of investors will disappear. After the results of the first quarterly report were announced, Aauto Quicker’s share price plummeted.

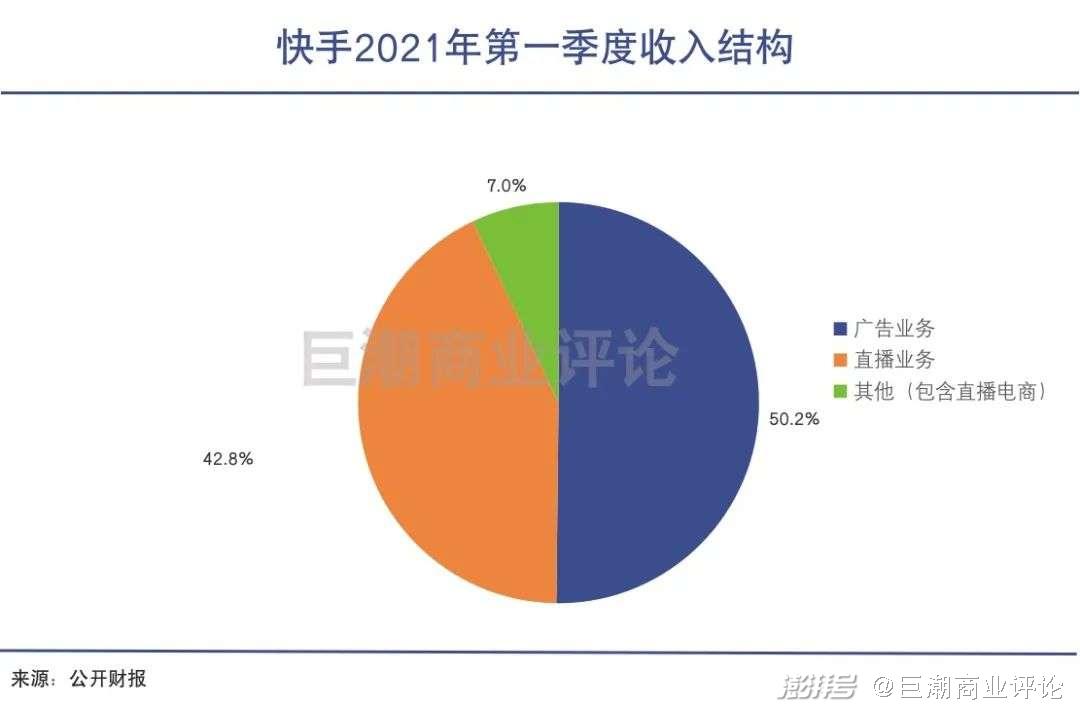

Judging from the data disclosed in the first quarterly report, the situation of commercial efficiency development in Aauto Quicker is mixed, which does not exceed market expectations: the outstanding performance is that advertising revenue is 8.56 billion yuan, up 161% year-on-year; The total amount of e-commerce transactions reached 118.6 billion yuan, a year-on-year increase of 219.8%.

However, there are hidden concerns in the live broadcast business: in the case of increasing daily activities and monthly activities, the revenue dropped by 19.5% year-on-year to only 7.3 billion yuan. The payment rate of live broadcast has also dropped from 14% in the peak period to 10% in this quarter.

Although the e-commerce business has a high growth rate of GMV, its monetization rate is much lower than the current mainstream e-commerce platform because the platform has given certain subsidies and rebates to sellers. If 1.2 billion yuan from other service businesses including e-commerce is counted as a platform draw, then the monetization rate of e-commerce in Aauto Quicker in the first quarter is only 1%. According to this ratio, even if the GMV of e-commerce exceeds 1 trillion this year, the corresponding income is only 10 billion yuan.

It can be predicted that in the future, when the live broadcast business has reached the ceiling, Aauto Quicker’s revenue will mainly come from advertising revenue, the growth of e-commerce GMV and the increase of e-commerce proportion.

As far as we can see, whether it’s e-commerce business or advertising revenue, the shaking of hands has given Aauto Quicker an invisible ceiling. In April this year, Bloomberg reported that the daily living in Tik Tok will reach 680 million in 2021, which is about 2.3 Aauto Quicker.

In terms of e-commerce business, according to public information, the GMV of e-commerce in Tik Tok will exceed 500 billion yuan in 2020, while that in Aauto Quicker will be nearly 400 billion yuan.

In advertising business, Tik Tok’s revenue in the first quarter exceeded 31 billion, about 3.6 times that of Aauto Quicker. Due to the large proportion of private domain weight in Aauto Quicker, users have plenty of time to refresh their "attention pages", which leads to their per capita Feeds being lower than that in Tik Tok, and there is less room for realizing advertisements.

Under the invisible ceiling of Tik Tok, in the next one to two years, it is easy for the capital market to form a more accurate expected upper limit for Aauto Quicker’s income growth.

For investors, this means that it is difficult for the market to make mistakes and it is difficult for investors to have opportunities for excess returns; For Aauto Quicker, there is still a lot of homework to be done to break through this ceiling, both in terms of user growth and commercialization efficiency.